Try a FREE Board Survey and get a Benchmarked Report - Click Here

APRA’s June 2026 draft revision of CPS 510 represents the most significant overhaul of prudential governance requirements in more than a decade. One of the key reforms is the consolidation of the existing CPS 510 (Governance), which applies to banks and insurers, and SPS 510 (Governance), which applies to superannuation trustees, into a single prudential standard. The new CPS 510 will establish a more consistent governance framework across APRA-regulated financial institutions.

The proposed standard forms part of APRA’s broader Governance Review, which commenced with its March 2025 Discussion Paper. Following extensive industry consultation and submissions, APRA released draft CPS 510 in June 2026. Consultation closes on 28 August 2026, with final standards and guidance expected later in 2026 and commencement proposed for early 2028. Although implementation remains some time away, boards should view 2027 as a critical preparation year.

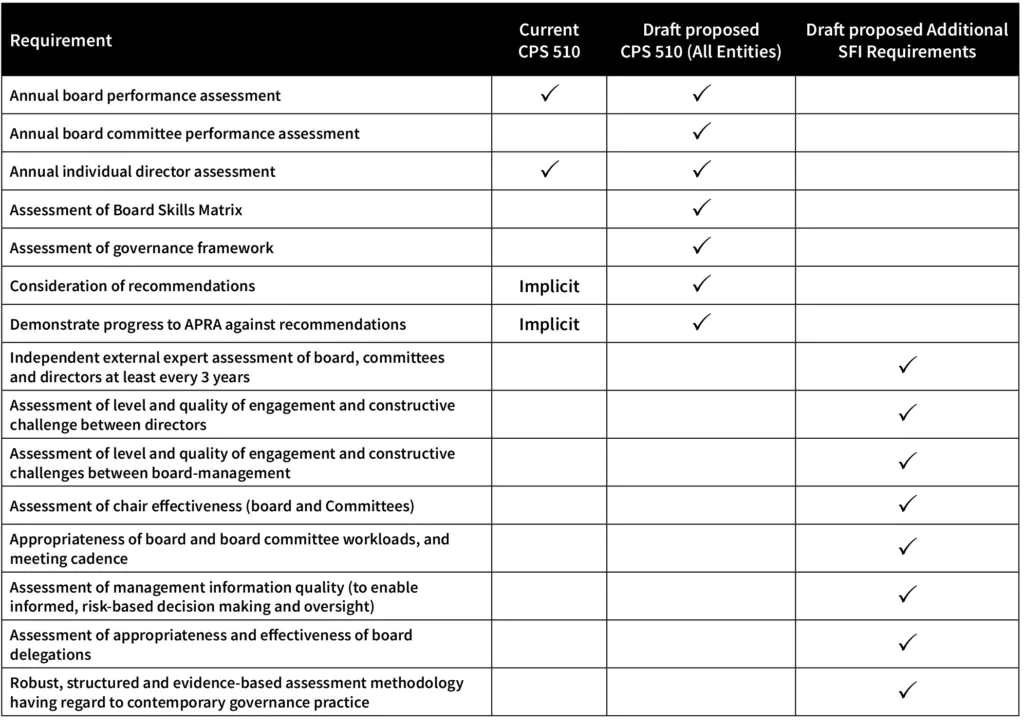

One of the most significant practical implications of the draft is the expansion of the requirements relating to board performance assessments.

APRA’s current requirement for board performance assessments occupies just 42 words. Its June 2026 draft revision of CPS 510 expands this to almost 400 words across seven separate provisions.

The significance of the proposed changes lies not simply in the number of new requirements, but in the level of prescription they introduce. Rather than requiring boards to conduct annual performance assessments, APRA is increasingly prescribing what must be assessed, the factors that must be considered and the evidence boards must be able to provide to demonstrate governance effectiveness and continuous improvement.

While this article focuses on board performance assessments, the draft CPS 510 also includes proposed changes relating to board capability, skills matrices, board renewal, fit and proper assessments, conflicts management and governance frameworks. A common theme across the reforms is APRA’s increasing focus on governance effectiveness and demonstrable outcomes rather than compliance with governance processes alone.

All APRA-regulated entities will be subject to the new annual performance assessment requirements in paragraphs 50–52. Significant Financial Institutions (SFIs) will be subject to additional requirements in paragraphs 53–56, including mandatory independent external board performance assessments at least every three years. The table below sets out the full picture.

For SFIs, the three-year external review is not new in concept. Many already engage external reviewers. What is new is the prescribed scope and the methodology required.

The independent review must additionally examine: the level and quality of constructive challenge between directors and between directors and senior management; the effectiveness of the chair and committee chairs; appropriateness of workloads and meeting cadence; the quality of management information; the appropriateness of board delegations; and progress against recommendations from the previous independent review.

The methodology in the draft standard is equally explicit. The review must be robust, structured, and evidence-based, informed by a range of perspectives, and have regard to contemporary governance practice. That last phrase carries more weight than it might appear to. Having regard to contemporary governance practice means the reviewer must know what good looks like in practice; across entities, sectors, and governance contexts. The risk is not that the review finds nothing wrong. The risk is that it finds nothing that the board did not already expect – leaving genuine weaknesses unexamined and recommendations confined to the comfortable.

SFIs will need to assess whether their current reviewer is sufficiently qualified and their current approach robust enough to satisfy what APRA now expects. APRA has indicated it will provide more details following consultation on the draft standard

The draft proposed standard also closes the gap in terms of what needs to happens after the review. The board must consider the assessment report and any resulting recommendations. Critically, the entity must be able to demonstrate to APRA progress against accepted recommendations.

This transforms the board review from a point-in-time event into an ongoing accountability mechanism. A board that accepts recommendations and then fails to track or demonstrate implementation now has a specific regulatory exposure it did not have before. Review outcomes need to be managed with the same rigour a board would expect of management responding to an internal audit finding.

The most useful question to ask now is whether your current review process would satisfy the draft standard if APRA examined it today.

For regulated entities, that means testing whether the annual assessment covers the full scope now required – governance framework effectiveness, skills matrix appropriateness, committee performance, and whether there is a process for tracking and demonstrating progress against recommendations.

For SFIs, the preparation task is larger. It means assessing whether the current external review approach is sufficiently structured, evidence-based, and capable of addressing APRA’s expanded expectations around constructive challenge, management information quality, delegations, and board-management dynamics.

The direction APRA is moving in is clear. Boards that use the transition period to build genuinely robust review processes will be much better placed than those that treat the commencement date as the starting gun.

To see a side-by-side view of the current and proposed provisions of CPS 510 click here.

Board Benchmarking

Australia

Level 27, 367 Collins Street

Melbourne, Victoria 3000

PH: +61 3 9909 9295

Westlake Governance

New Zealand

PO Box 8052

Wellington 6140

New Zealand

PH: +64 21 443 137

Halex Consulting

United Kingdom

86-90 Paul Street London, EC2A 4NE

PH: +44 (0)20 3823 6569

Cornerstone

India

313 Gokul Arcade

Subhash Road,

Vile Parle East

Mumbai, 400057

PH: +91 981 907 7135

Peakstone Global

Australia

GPO Box 1486

Brisbane Queensland 4001

PH: 1300 860 450

Board Benchmarking

Malaysia

66 Jalan Ibrahim Johor Bahru

80000 Johor

PH: +60 1933 54731

BDO

Mauritius

10 Frère Félix de Valois

Port Louis

PH: +230 202 3000

Gaines Advisory

Australia

PO Box 610

Cottesloe WA 6011

PH: +61 414 633 230

BDO

Malaysia

360 Jalan Tuanku Abdul

Rahman

50100 Kuala Lumpur

PH: +603 2616 2888

Twafiika Consultants

Africa

20 Eugmbo Street

Windhoek

Namibia

PH: +264 81 287 2104